Why Credit Unions Must Balance AI Chatbots with Human Trust

A critical examination of AI chatbots, warning credit unions against overreliance on tech that erodes human trust and member loyalty across all ages—including among Millennials and Gen Z

Live Chat: Members texting in real-time with a human member services representative—people helping people—on credit union websites and apps.

AI Chatbot: Members texting with an artificial intelligence-powered computer program that’s imitating live human interaction on credit union websites and apps. Members are chatting with a robot—hence, a chatbot. A conversational generative AI chatbot is a type of AI that creates answers that are as human-like as possible. While simpler chatbots exist, all replace live people as the means of communication with members.

Using technology in the right areas is key for member satisfaction, but not where it’s unpopular with members. No credit union wants to transform member interactions from friendly human experiences into frustrating dystopian nightmares.

According to the Declaration of Independence, it is a self-evident truth that all humans are created equal and are endowed by their Creator with certain unalienable rights. This affirms the unique worth of human beings. No advanced technology will ever match the value of human connection: Would you replace your children with ultra-realistic robots? Would you swap your friends and family for advanced droids? R2-D2 is cool, but not as cool as Han Solo. Do you want AI-generated characters to replace your favorite human actors in movies and TV shows? Do credit union members, including younger ones, want AI chatbots to replace human representatives?

Recent insights from Gen Z suggest the answer is no. At the 2023 Money20/20 Underground Collision event, Denise Wymore reported, “Lenny Vallone, CMO of SCE FCU, invited five Gen Z finance majors from the UNLV Runnin’ Rebels to speak to the credit union executives in attendance about their views on credit unions, banking, and finance in general.”1 Two key takeaways were: first, Gen Z demands the latest technology in smartphone apps; second, they don’t want technology replacing human interaction. As Wymore states, “they also crave a human connection. They are not big fans of chatbots and don’t want to transact digitally 100 percent of the time. Surprisingly, they feel that a branch presence is necessary.”2

A recent Credit Union Times article, “Conversational Chat AI: A Strategic Imperative for Retaining Millennial & Gen Z Members,” claims AI chatbots are vital for engaging young members.3 The article begins by citing vague “industry data” claiming “only about 4% of Gen Z and 5% of Millennials currently belong to a credit union.” It then cites an unidentified “recent J.D. Power study” stating “31% of members under 40 say they are likely to leave their credit union within the next 12 months, often citing fees and slow service as catalysts.”4 The article’s “strategic takeaway” is that conversational generative AI chatbots are a “core engagement layer” to fix credit unions’ youth problem by “speaking the digital language younger members expect.”5 It’s worth noting that the article’s author, Jack Chawla, is VP of Marketing for an AI solutions provider for credit unions and community banks.6

As mentioned, Chawla’s credit union membership figures—4% for Gen Z and 5% for Millennials—are based on “industry data.” His source appears to be a 2023 article by Keypoint Intelligence, which provides no hyperlink to the original research report.7 As an aside, Keypoint Intelligence never mentions AI or chatbots. Other reliable sources report higher figures for younger people who use credit unions as their primary financial institution. McKinsey & Company reports 10% for Gen Z and 21% for Millennials.8 Apiture finds 14% for Gen Z and 20% for Millennials.9 Again, these numbers represent their choice of primary financial institution. When Chawla’s criterion of simply belonging to a credit union is considered, higher numbers can be found. For example, a GoBankingRates survey found that “about 26% of Gen Z already use credit unions for their banking.”10 That’s considerably higher than the “about 4%” Chawla gives. While it’s true that credit unions need more younger members, it’s also true that the credit union youth apocalypse is not upon us.

What can credit unions do to attract younger members? According to Apiture, “30% of Gen Z and 21% of millennials aren’t even aware they can join a credit union.”11 It further adds that there’s opportunity for change, with 47% of Gen Z and millennials willing to switch to a credit union.”12 These figures suggest that younger generations’ lack of awareness hinders credit unions more than a lack of AI chatbots. As Matthew DiGangi, a MassMutual executive, has stated, “In general, young people have less exposure to and understanding of credit unions than previous generations.”13 Yet, reasons for optimism exist. For example, a 2023 LendingTree-sponsored survey of more than 2,000 U.S. consumers found that Gen Z is “the most likely age group to prefer credit unions.”14 The same study states 77% of Americans who choose credit unions over banks report “being the most satisfied of any institution type with their service.”15 Credit unions should focus on awareness campaigns to young people rather than eroding their customer service advantage over banks by replacing human representatives with AI chatbots.

What about the unidentified “recent J.D. Power study” Chawla mentions? It is almost certainly the 2025 U.S. Credit Union Satisfaction Study. It does state “31% of members under age 40 say they ‘probably will’ or ‘definitely will’ leave their credit union in the next 12 months.” However, its public key findings link this attrition risk solely to “the fees they were charged,”16 not due to AI chatbot needs or “slow service,” as Chawla implies and suggests.17 The study goes on to rank SchoolsFirst Federal Credit Union highest in member satisfaction.18 This is noteworthy, as SchoolsFirst Federal Credit Union’s website exclusively uses human Live Chat, not AI chatbots.19 The same is true for other large, highly rated credit unions like Golden1 Credit Union.20

In the interest of fairness, it should be noted that the study’s second and third-highest-ranked credit unions, Idaho Central Credit Union and Navy Federal Credit Union, respectively, do use AI chatbots. However, these chatbots are deeply integrated with real humans via Live Chat. Idaho Central Credit Union has an initial chatbot, but it can quickly transfer to Live Chat. It even offers “face-to-face” conversations with a live service agent through ICCU’s VideoChat.”21 Navy Federal Credit Union offers Live Chat during business hours and an AI chatbot (virtual assistant) for 24/7 help.22 The study also states, “Credit unions outperform their retail bank counterparts across all dimensions measured in the study, including trust, people, and problem resolution.”23 This refutes Chawla’s “strategic takeaway” that credit unions risk being left behind by their competitors if they delay implementing AI chatbots.24 Credit unions are trusted over banks because their people (not AI chatbots) resolve members’ problems.

Chawla’s “strategic takeaway” that AI chatbots speak “the digital language younger members expect” is dubious.25 As stated earlier, Gen Zers at the 2023 Money20/20 Underground Collision event preferred human connection over chatbots. Furthermore, McKinsey & Company’s “Where Is Customer Care in 2024?” states that a recent survey of 3,500 consumers, respondents of all ages, said that live phone conversations were among their most preferred methods of contacting companies for help and support. That finding held true even among 18- to 28-year-old Gen Z consumers, a cohort that favors text and social messaging for interpersonal communications.”26 It adds, “There’s also evidence that younger consumers are getting tired of the digital self-service paradigm. One financial-services company reports that its Gen Z customers are 30 to 40 percent more likely to call than Millennials, and they use the phone as often as baby boomers.”27 It adds, “57 percent of leaders expect call volumes to increase by as much as one-fifth over the next one or two years.”28 Just as video did not kill the radio star, with over 80% of Americans listening weekly,29 AI chatbots won’t kill the live member services representative.

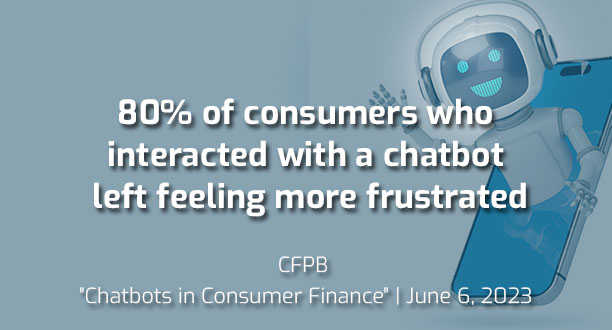

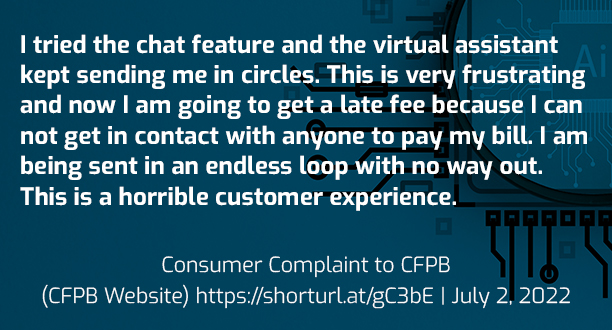

These figures indicate that people of all ages value human support—whether by phone or chat—and that AI chatbots are often disliked. The CFPB’s “Chatbots in Consumer Finance” reports “80% of consumers who interacted with a chatbot left feeling more frustrated, and 78% needed to connect with a human after the chatbot failed to serve their needs.”30 It cites complaints about “doom loops.”31 It warns that chatbots risk “violating legal obligations, eroding customer trust, and causing consumer harm,” and they “can also raise certain privacy and security risks.”32 It specifically calls out “conversational, generative chatbots” as “not well-positioned to distinguish between factually correct and incorrect data.”33 According to a July 2024 Gartner Data & Analytics Summit, “At least 30% of generative AI (GenAI) projects will be abandoned after proof of concept by the end of 2025, due to poor data quality, inadequate risk controls, escalating costs, or unclear business value.”34 It further states that “After last year’s hype, executives are impatient to see returns on GenAI investments,”35 adding that “these deployment approaches come with significant costs, ranging from $5 million to $20 million.”36

Other claims in Chawla’s article lack sources and methodology and can’t easily be vetted.37 Some data resembles self-reported figures from his company website’s “Case Studies” page—stories of credit unions successfully implementing AI solutions, including chatbots.38 Such data should be carefully weighed.

For example, consider its case study of Pasadena Service Federal Credit Union (PSFCU). Chawla’s company began its partnership with PSFCU in 2021.39 The case study’s outcome was that PSFCU implemented an AI chatbot for 24/7 support that contributed to “transforming their service model from digital-first to AI-first.”40 However, the case study itself acknowledges it is outdated, as PSFCU merged with Pasadena Federal Credit Union (PFCU) in March 2024.41 PFCU is the active credit union.42 PSFCU is inactive.43 Its former URL, mypsfcu.org, now points to a Vietnamese website that streams foreign soccer games.44 The outdated nature of this case study is relevant, as will be shown below.

Interestingly, the “AI-first” chat model that PSFCU started in 2021 is not the model that PFCU uses in 2025, even though the same CEO was in charge during both timeframes.45 A 2024 PFCU Facebook post states that “We chose to have our online chat to feature live agents instead of just a chatbot” and that “You actually talk to humans when you use our Pasadena FCU Live Chat!”46 Their Live Chat is always available during its business hours and even features a photo of the human agent in the chat window.47 Yet, on Chawla’s company blog, he states, “With AI Chat so advanced, maybe Live Chat is not something even worth investing in.”48 It’s difficult to reconcile his statement with the fact that one of his company’s AI-first chat case study participants is now advocating for human-first Live Chat. Adding that to the fact that the highest-ranked credit unions are heavily invested in Live Chat in one way or another makes reconciling his statement almost impossible.

As stated earlier, technology is key to member satisfaction, and AI plays a role. Predictive AI aids backend tasks like fraud detection and prevention.49 Basic AI chatbots for simple questions—like an FAQ page on steroids, with a quick and easy offramp to a live agent—may or may not enhance websites and apps.50 However, replacing human staff with AI chatbots as the primary chat function risks eroding the trust that defines the ethos of credit unions. All credit unions want to live up to the motto, “people helping people.” No credit union wants to be known for “AI chatbots frustrating people.” When it comes to heavily relying on AI chatbots to communicate with members, as the old adage goes, “just because you can, doesn’t mean you should.”

Endnotes:

- Denise Wymore, “What the future generation thinks about credit unions“, zest.ai, December 06, 2023, para. 1. https://www.zest.ai/learn/blog/future-generation-credit-unions/ ↩︎

- Denise Wymore, “What the future generation thinks about credit unions“, para. 8. ↩︎

- Jack Chawla, “Conversational Chat AI: A Strategic Imperative for Retaining Millennial & Gen Z Members”, Credit Union Times, June 30, 2025, https://www.cutimes.com/2025/06/30/conversational-chat-ai-a-strategic-imperative-for-retaining-millennial–gen-z-members/ ↩︎

- Chawla, “Conversational Chat AI: A Strategic Imperative for Retaining Millennial & Gen Z Members“, para. 1. ↩︎

- Chawla, “Conversational Chat AI: A Strategic Imperative for Retaining Millennial & Gen Z Members“, para. 13. “Conversational” is used synonymously with “generative” in Chawla’s article (e.g., its subtitle: “Conversational chat AI, implemented as an end-to-end generative platform.”) ↩︎

- Chawla, “Conversational Chat AI: A Strategic Imperative for Retaining Millennial & Gen Z Members“, author bio ↩︎

- Andy Young, “What Do Younger Consumers Look for in a Financial Services Provider?” Keypoint Intelligence, April 27, 2023, para. 7. https://whattheythink.com/articles/114866-what-do-younger-consumers-look-financial-services-provider/ ↩︎

- McKinsey & Company, “Credit unions’ Youth Dilemma”, mckinsey.com, July 10, 2024, graph, https://www.mckinsey.com/featured-insights/sustainable-inclusive-growth/charts/credit-unions-youth-dilemma ↩︎

- Apiture, “Half of Gen Z and Millennials Open to Switching Primary Financial Institution to a Community Bank, Online-Only Bank, or Credit Union, New Apiture Study Finds”, Apiture.com, June 13, 2024, para. 3. https://www.apiture.com/half-of-gen-z-and-millennials-open-to-switching-primary-financial-institution-to-a-community-bank-online-only-bank-or-credit-union-new-apiture-study-finds/ ↩︎

- Nicole Haverly, “Closing the Digital Divide: Credit Unions Should Prioritize Tech Over Transactions“, The Financial Brand, March 6th, 2025, https://thefinancialbrand.com/news/banking-technology/closing-the-digital-divide-why-credit-unions-should-prioritize-tech-over-transactions-187186 ↩︎

- Jennifer Dimenna, “How Can Credit Unions Attract Younger Members?”, Apiture.com, November 19, 2024, para. 1. https://www.apiture.com/ways-credit-unions-can-attract-younger-members/ ↩︎

- Dimenna, “How Can Credit Unions Attract Younger Members?”, para. 4. ↩︎

- Nicole Spector, “Gen Z and Millennials Favor National and Online Banks, Survey Shows — What Does That Mean for the Future of Credit Unions?”, GoBankingRates, February 6, 2022, https://www.gobankingrates.com/banking/credit-unions/gen-z-millennials-favor-national-online-banks-survey-shows-what-does-mean-for-future-credit-unions/ ↩︎

- Maggie Davis, “National Banks Are the Most Popular With Consumers, But They Don’t Generally Offer the Best Rates — Find Out Where Your Money Could Grow the Most“, DepositAccounts by Lendingtree, March 06, 2023, 3rd bullet point under graph, https://www.depositaccounts.com/blog/bank-sizes-study-survey.html ↩︎

- Maggie Davis, “National Banks Are the Most Popular With Consumers, But They Don’t Generally Offer the Best Rates — Find Out Where Your Money Could Grow the Most“, para. 5. ↩︎

- J.D. Power Press Release, “Trust and Convenience Drive Satisfaction with Credit Unions but Overdraft Fees Present Risks, J.D. Power Finds“, jdpower.com, April 1, 2025, para. 4., https://www.jdpower.com/business/press-releases/2025-us-credit-union-satisfaction-study ↩︎

- Chawla, “Conversational Chat AI: A Strategic Imperative for Retaining Millennial & Gen Z Members“, para. 1. ↩︎

- J.D. Power, “Trust and Convenience Drive Satisfaction with Credit Unions but Overdraft Fees Present Risks, J.D. Power Finds”, para. 7. ↩︎

- SFFCU Live Chat. Accessed August 5, 2025. https://www.schoolsfirstfcu.org/contact/get-in-touch/contact-us/ ↩︎

- J.D. Power, Golden1 Credit Union ranked 10th on the graph.; Live Chat: https://www.golden1.com/contact-us ↩︎

- ICCU Chatbot/Live Chat & Video Chat. Accessed August 5, 2025. https://www.iccu.com/contact/ ↩︎

- NFCU. Live Chat/Virtual Assistant. Accessed August 5, 2025. https://www.navyfederal.org/contact-us.html ↩︎

- J.D. Power, “Trust and Convenience Drive Satisfaction with Credit Unions but Overdraft Fees Present Risks, J.D. Power Finds”, para. 3. ↩︎

- Chawla, “Conversational Chat AI: A Strategic Imperative for Retaining Millennial & Gen Z Members“, para. 13. ↩︎

- Chawla, “Conversational Chat AI: A Strategic Imperative for Retaining Millennial & Gen Z Members“, para. 13. ↩︎

- McKinsey & Company, “Where Is Customer Care in 2024?”, mckinsey.com, March 12, 2024, para. 9., https://www.mckinsey.com/capabilities/operations/our-insights/where-is-customer-care-in-2024 ↩︎

- McKinsey & Company, “Where Is Customer Care in 2024?”, para. 10. ↩︎

- McKinsey & Company, “Where Is Customer Care in 2024?”, para. 8. ↩︎

- Naomi Forman-Katz, “For National Radio Day, Key Facts About Radio Listeners and the Radio Industry in the U.S.”, Pew Research Center, August 17, 2023, para. 2., https://www.pewresearch.org/short-reads/2023/08/17/for-national-radio-day-key-facts-about-radio-listeners-and-the-radio-industry-in-the-us/ ↩︎

- Consumer Financial Protection Bureau, “Chatbots in Consumer Finance,” ConsumerFinance.gov, June 6, 2023, Hindering access to timely human intervention, para. 1, https://www.consumerfinance.gov/data-research/research-reports/chatbots-in-consumer-finance/chatbots-in-consumer-finance/ ↩︎

- CFPB, “Chatbots in Consumer Finance,” Failure to provide meaningful customer assistance, para. 1. ↩︎

- CFPB, “Chatbots in Consumer Finance,” Executive summary, para. 5. ↩︎

- CFPB, “Chatbots in Consumer Finance,” Providing inaccurate, unreliable, or insufficient information, para. 2. ↩︎

- Gartner Press Release, “Gartner Predicts 30% of Generative AI Projects Will Be Abandoned After Proof of Concept By End of 2025“, Gartner.com, July 29, 2024, para. 1., https://www.gartner.com/en/newsroom/press-releases/2024-07-29-gartner-predicts-30-percent-of-generative-ai-projects-will-be-abandoned-after-proof-of-concept-by-end-of-2025 ↩︎

- Gartner, “Gartner Predicts 30% of Generative AI Projects Will Be Abandoned After Proof of Concept By End of 2025“, para. 2. ↩︎

- Gartner, “Gartner Predicts 30% of Generative AI Projects Will Be Abandoned After Proof of Concept By End of 2025“, para. 3. ↩︎

- Chawla, “Conversational Chat AI: A Strategic Imperative for Retaining Millennial & Gen Z Members“, para. 13. States with no source: “Early adopters report containment rates above 70%” ↩︎

- “Bank of Guam Taps Generative AI to Scale Digital-First Support.” Self-reported, no methodology key result: “76% chat containment“, Interface.ai. Accessed August 5, 2025. https://interface.ai/case-studies/bank-of-guam/ ↩︎

- CUInsight Press Release, “Pasadena Service Federal Credit Union partners with interface.ai to significantly enhance member experiences & operational efficiencies by offering an intelligent virtual assistant“, cuinsight.com, May 26, 2021, https://www.cuinsight.com/press-release/pasadena-service-federal-credit-union-partners-with-interface-ai-to-significantly-enhance-member-experiences-operational-efficiencies-by-offering-an-intelligent-virtual-assistant/ ↩︎

- interface.ai PSFCU Case Study, “Pasadena Service Federal Credit Union Deploys AI to Provide Instant, Omnichannel Member Support.” Interface.ai. Accessed August 5, 2025. para. 2. https://interface.ai/case-studies/pasadena-service-federal-credit-union/ ↩︎

- interface.ai PSFCU Case Study, “Pasadena Service Federal Credit Union Deploys AI to Provide Instant, Omnichannel Member Support.” Accessed August 5, 2025. para. 3. ↩︎

- PFCU active status on NCUA, https://mapping.ncua.gov/CreditUnionDetails/594 ↩︎

- PSFCU inactive status on NCUA, https://mapping.ncua.gov/CreditUnionDetails/1368 ↩︎

- mypsfcu.org points to https://www.carlyscafe.com/, which points to XOILAC TV. Accessed August 5, 2025. https://www.mypsfcu.org ↩︎

- James Chang was CEO of PSFCU, https://mapping.ncua.gov/CreditUnionDetails/1368; He is currently CEO of PFCU, https://mapping.ncua.gov/CreditUnionDetails/594 ↩︎

- Pasadena FCU‘s post, December 18, 2024, https://www.facebook.com/pasadena.fcu/posts/did-you-know-you-are-actually-chatting-to-one-of-our-member-representatives-when/1143352721130574/ ↩︎

- Pasadena FCU‘s Let’s Chat! Feature. Accessed August 5, 2025. https://www.pfcu.org/ ↩︎

- Jack Chawla, “Advanced AI Chat: The Future of Digital Member & Customer Interaction“, Interface.ai, April 8, 2025, Last sentence. Accessed August 5, 2025. https://interface.ai/advanced-ai-chat-the-future-of-digital-member-customer-interaction/ ↩︎

- Charles James, “Predictive Analytics in Financial Fraud Detection and Prevention“, researchgate.net, December 23, 2021, https://www.researchgate.net/publication/387582908_Predictive_Analytics_in_Financial_Fraud_Detection_and_Prevention ↩︎

- CFPB, “Chatbots in Consumer Finance,” para. 4. ↩︎