Why Would People Throw Money Away with Banks Instead of Investing in a Credit Union?

It can be in search of a checking account, a savings account, or a loan (such as that first mortgage) that drives a person to sign up for their first account at a financial institution, and oftentimes, they go straight to the big banks, not knowing the cost of admission beyond the extremely effective advertising campaigns. Big banks are successful because they make so much revenue from their customers. Oftentimes, friends and family members will be seen and heard complaining or struggling with high fees and monthly service charges, and more and more with no known recourse, and having to accept that this is part of the financial journey! Let’s look more into the differences between credit unions vs. banks.

Credit Unions and Loans

One of the first loans that most people tend to go for is the auto loan, and as a credit union, you can be that first direct or private party loan for a member. It would seem that a person seeking a loan for a car is more inclined to accept whatever loan they get from the dealer, but oftentimes, that is just as wasteful as getting a loan from a bank. A member of a credit union is often more likely to find better rates and acceptance for loans from their credit union, and that can save a lot of money on interest, fees, and other charges. Since members are not only customers but owners vested in the growing concern of the credit union, it means they are investing in their own “business.”

Credit unions are more likely to take a risk for a loan with a member than a bank would be with a customer. This is why many would be willing to say that it is easier to get approved for a loan with a credit union than with a bank. For auto loans, we have seen a rise in auto lenders undercutting the banks and credit unions, but an auto loan with a credit union comes with other benefits that are more than just purchasing a car for an impossibly low rate. It builds a relationship with that credit union, and when members are ready for their next credit card, mortgage, or business loan, this can be all the difference in getting the loan.

A major focus of a credit union is to provide essential services and lending opportunities when your members need them most. As great as credit unions are with benefits and consistently low rates, it is almost impossible to operate without any revenue when providing unbeatable rates 24/7/365. This means that strategizing lending rate drops and promotional loans, home equity lines, and other services are essential to provide members with outstanding opportunities, keep up the revenue stream, and propel the credit union into the future! Strategy for promotional efforts can depend heavily on your field of membership, and when you analyze lending spikes! For example, some credit unions might see higher auto lending applications around Memorial Day in their communities. Or you can provide great consumer lending rates during the holidays!

Credit Union Members

Finding opportunities to connect with your members and provide the best services at the best rates at the best times is what makes the credit union different and drives trust and loyalty! Especially since most, if not all, credit unions tend to work off of the “3 Stakeholder Rule.” They are the members, the employees, and the credit union that they are concerned with, and many have learned that the more they look to the needs and wants of the employees and members, the credit union’s growing concern will be met. Banks tend to focus on the bottom line, and not so much on the people they employ or service.

Oak Tree keeps credit unions compliant and connected to their community growth through compliant forms and documents, and many other services! Browse our products today and start expanding your services and membership. When we originally posted the credit unions vs. banks infographic, it was well-received. We only ask that you credit us when sharing, and please don’t crop out our logo.

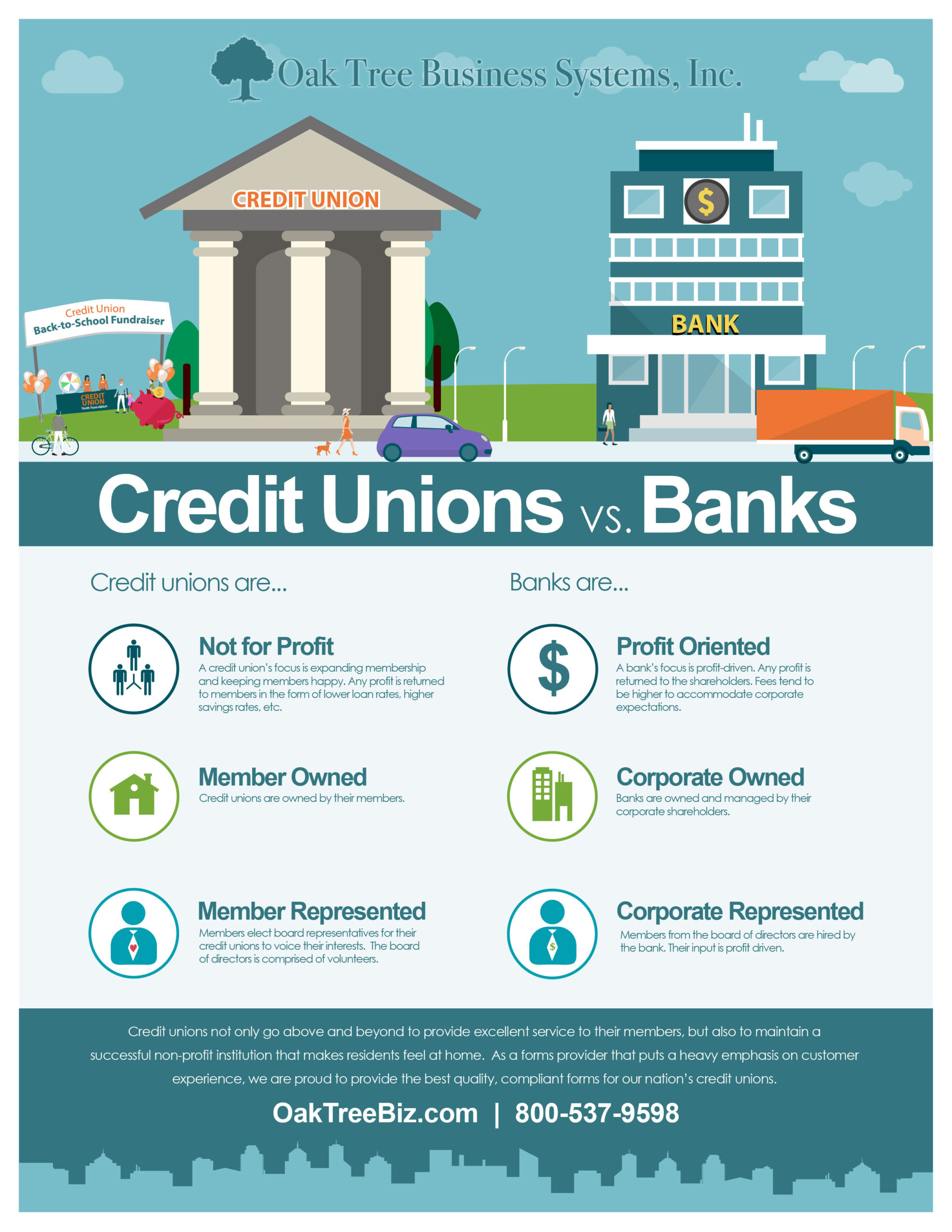

3 Big Bank vs. Credit Union Differences

Oak Tree is more than just a “vendor” to the credit unions we work with; we think of ourselves as partners. We work closely with the credit unions across America because we are a part of the Credit Union Community. Because of this affinity, we tend to help the credit union movement and talk about how credit unions can be a better choice for your financial institution choices. We have looked at the question of why people would throw their money away with a bank, but now we just wanted to put out the 3 big bank vs. credit union differences we think help differentiate these institutions.

Credit unions and banks offer similar services: they accept deposits into checking (Share Draft Accounts for credit unions) and savings (Share Accounts for credit unions) accounts, and make loans. However, the structure of these two financial institutions is very different. There are three main areas in which banks and credit unions vary greatly: Ownership, profit, and service.

Who’s in Charge Around Here?

You’re in charge! Well, at least if you’re part of a credit union, that is. Credit unions run on a democratic voting system—one member has one vote. For credit unions, it doesn’t matter how much money you have in your checking and savings accounts. As long as you belong to the credit union, you have an equal say in how things operate. In addition, individuals on the board of directors are all volunteers, are elected by the members, and are not paid. Any member of the credit union can run to become a board member. On the other hand, banks are run mostly by a paid board of directors. Board members are elected by shareholders. The more shares an individual has, the greater their voting power is, and the more “say” they have in how the bank operates.

For-Profit or Not-for-Profit?

This one is simple. Credit unions are not-for-profit, while banks are for-profit. Banks exist to earn profits for their shareholders. Because credit unions are not-for-profit, their earnings are passed on to their members by offering low-interest rates on loans and higher interest rates on savings accounts. In some instances, credit unions will offer free checking accounts. This profit orientation affects the type of loans and services that each financial institution offers.

Service Comes First

Credit unions mainly serve at the community level, which allows them to be more “in-tune” with their members’ needs. In addition, they serve those belonging to similar organizations, such as teachers, firefighters, airlines, and universities, etc.

By having members with common interests, credit unions have a better understanding of the wants and needs of their members, and therefore can better serve their interests. In addition, their size allows members to get to know the employees who work there, and members build important relationships that are beneficial when it comes time to apply for a loan. Credit unions are also part of a cooperative, which allows them to share resources with other credit unions, such as shared ATM network branching (allowing members to withdraw from other credit unions’ ATMs), and much, much more.

After comparing these two financial institutions, it is clear to see that the credit union’s mission is to better serve members and to improve members’ financial lives. Credit union members have reached a new high of over 122.3 million members in the United States as of 2020. By giving members the financial services that they really need, this number is certain to continue to rise as the beneficial reputation of credit unions continues to spread. Besides these 3 big bank vs. credit union differences, what other key differences helped you choose a cu over a bank?

(Note: this is a consolidation of two different posts.)